All Eyes on the Labor Market: 2024 Market Outlook

by Sequoia Financial Group

by Sequoia Financial Group

2023 Market Review

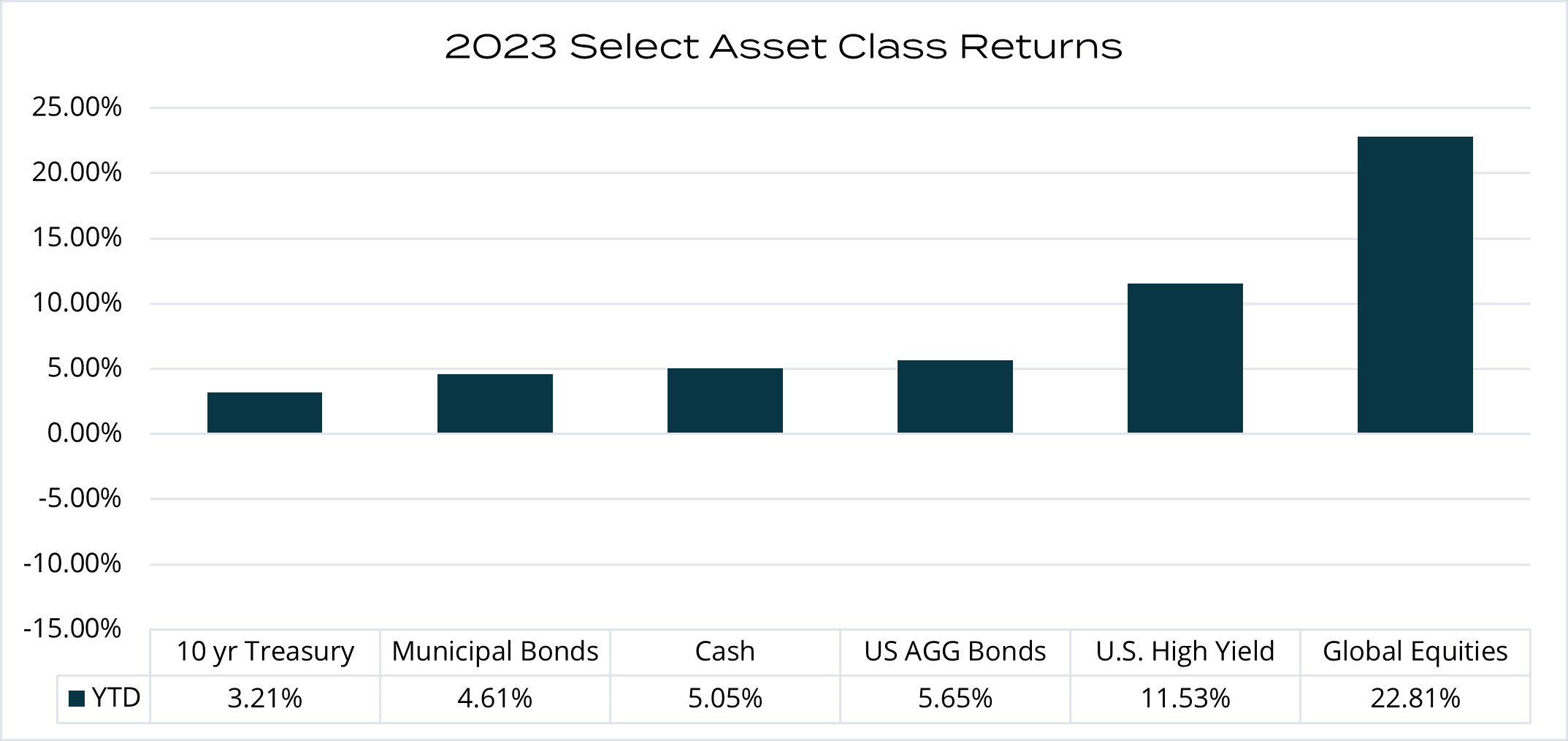

Looking back at the year that was, financial markets delivered broadly positive performance. Better than expected economic data paved the way for investors to embrace risk, with return-seeking assets outperforming defensive areas of the market.

For example, while cash or bond equivalents, which are among the most defensive of asset classes, had a banner year, with short-term rates exceeding 5%, those returns paled in comparison to global equities (the most traditional risky asset class), which returned 23% in 2023. This was not the year to hunker down in cash. U.S. equities, as measured by the S&P 500, finished the year near all-time highs.

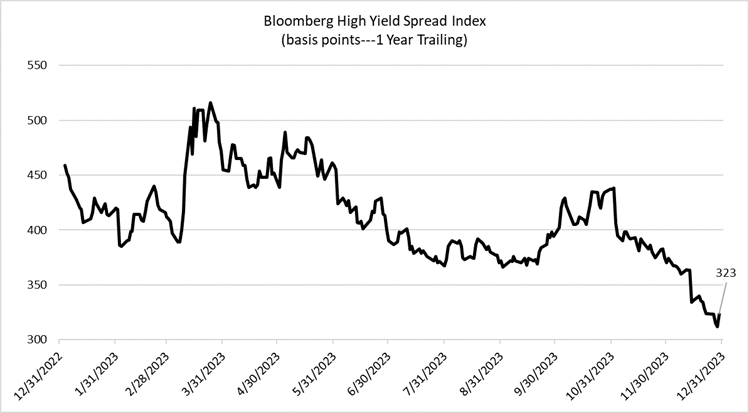

In addition, riskier (high yield) bonds represented the best-performing area of the fixed income market, as credit spreads (the premium demanded by investors for taking additional credit risk) narrowed throughout the year.

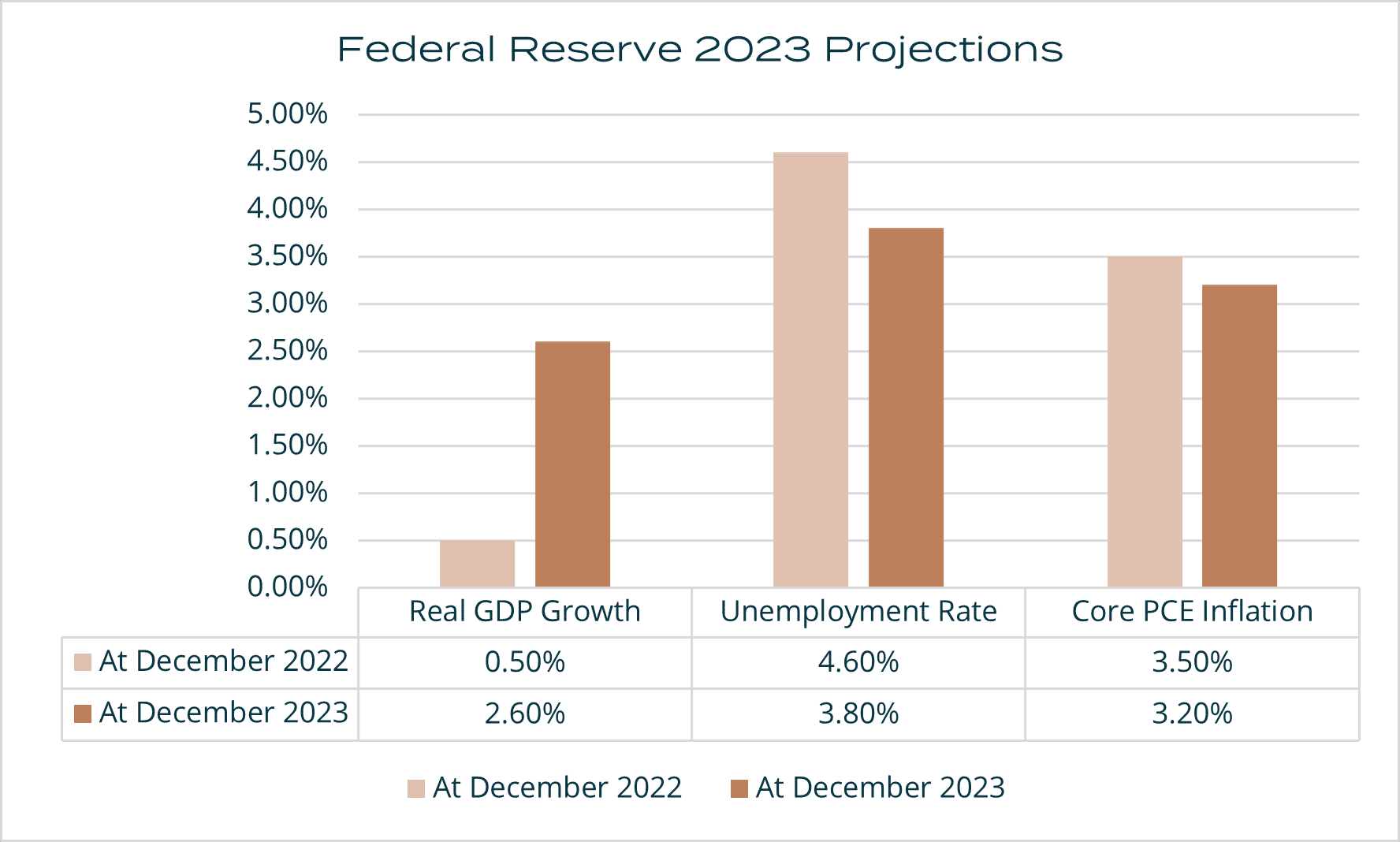

Encouragingly, economic activity (particularly within the service side of the economy) broadly outpaced low expectations heading into 2023. Policymakers pulled off the difficult task of reining in inflation by more than expected, while maintaining healthy economic growth and lower unemployment. The chart below depicts some of the Fed’s key economic projections for 2023. In December 2022, the Fed believed that a restrictive policy would lead to lower growth and higher unemployment. Many market prognosticators spent most of the year waiting for the U.S. consumer to buckle, which didn’t come to fruition, as the unemployment rate is expected to finish the year at just 3.8%.

If the labor market doesn’t weaken in 2024, the consumer (and the economy) may continue to outperform expectations. We suspect the most watched real-time economic indicator in 2024 will be the weekly unemployment claims data, because so much consumer activity is dependent upon the health of the labor market. The runway for the U.S. consumer is highly dependent upon employment trends … if everyone has a job who wants one, they will likely continue to spend.

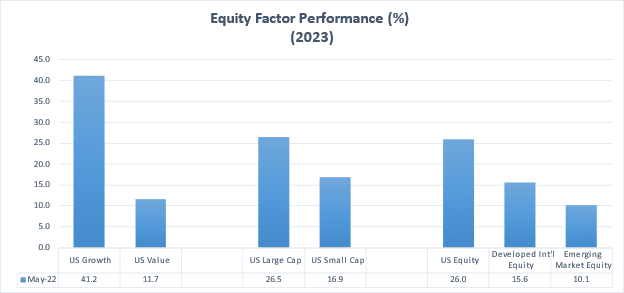

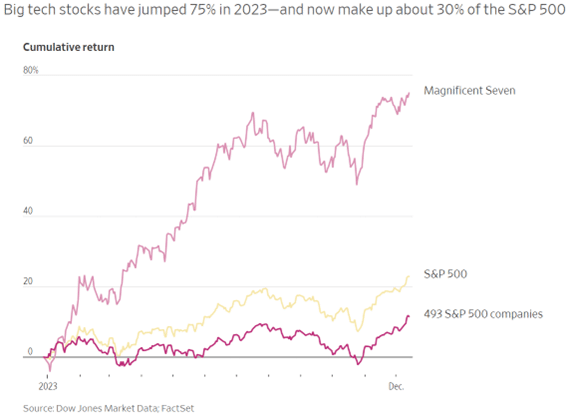

Style dispersion, which reflects the performance gap between growth and value stocks, was very wide in 2023, with growth-oriented investments outpacing value investments. More specifically, the demand for large cap U.S. growth stocks re-emerged in a big way in 2023.

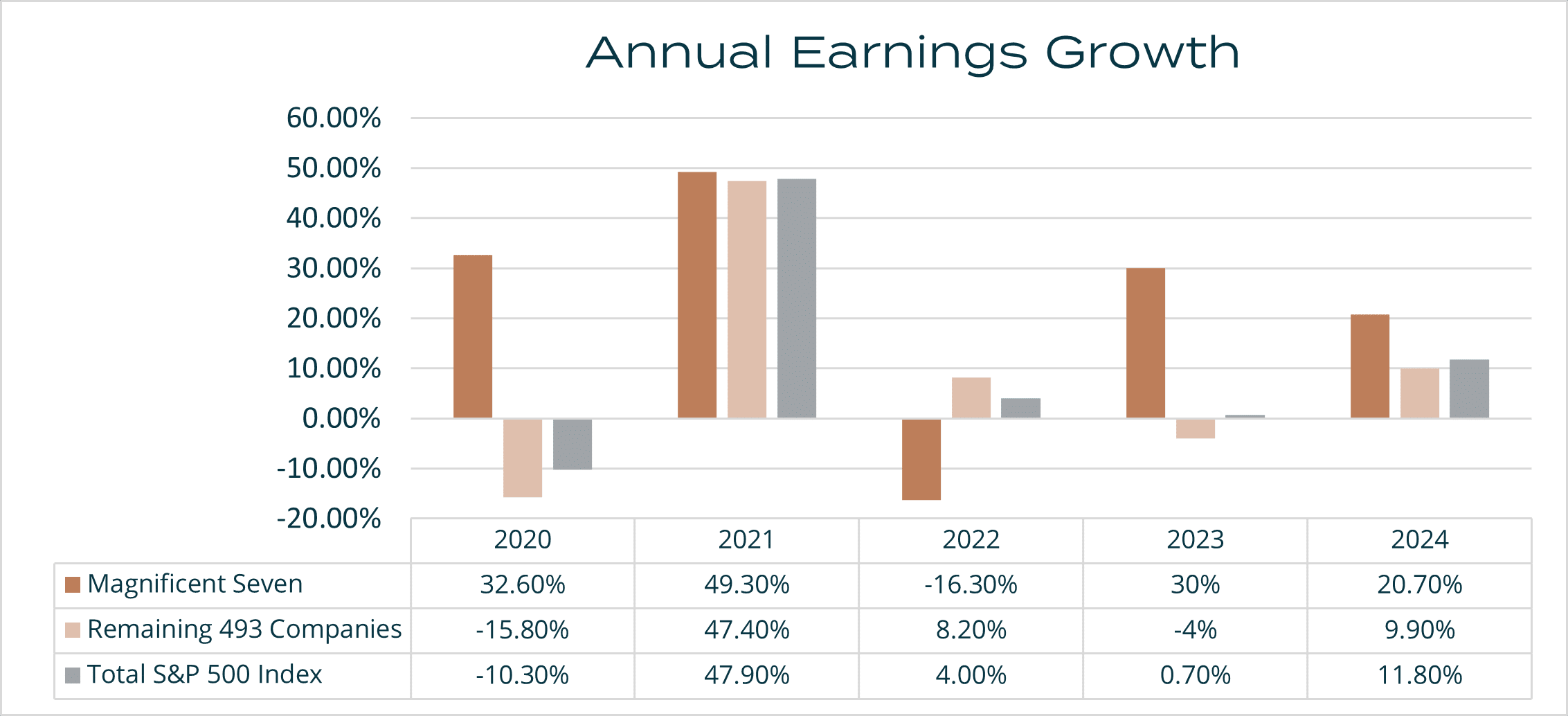

The earnings growth of what has become known as the “Magnificent 7” (Alphabet, Amazon, Apple, Meta Platforms, Microsoft, NVIDIA, and Tesla) proved to be much faster than the market expected heading into 2023, with various growth themes sparking market optimism. Per the chart below, the earnings growth of these seven stocks far outpaced the overall market, paving the way for a very concentrated source of equity market returns.

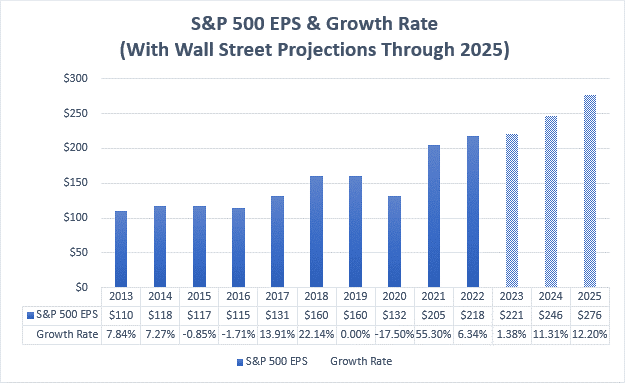

Overall, equity valuations expanded in 2023, with multiple expansion accounting for much of the equity market returns. Full year 2023 earnings growth for the S&P 500 looks to be coming in at about 1% compared to a total return of approximately 26% for 2023. However, relative to expectations, earnings came in far better than what many had anticipated heading into 2023.

Finally, within fixed income markets, credit outperformed duration, meaning that additional credit risk within fixed income investments paid off in 2023, with spreads tightening throughout the year. Lower credit spreads supported higher prices for higher-yielding fixed income investments. Taking additional risk paid off in 2023.

2024 Market Outlook

GDP Growth Expected to Slow

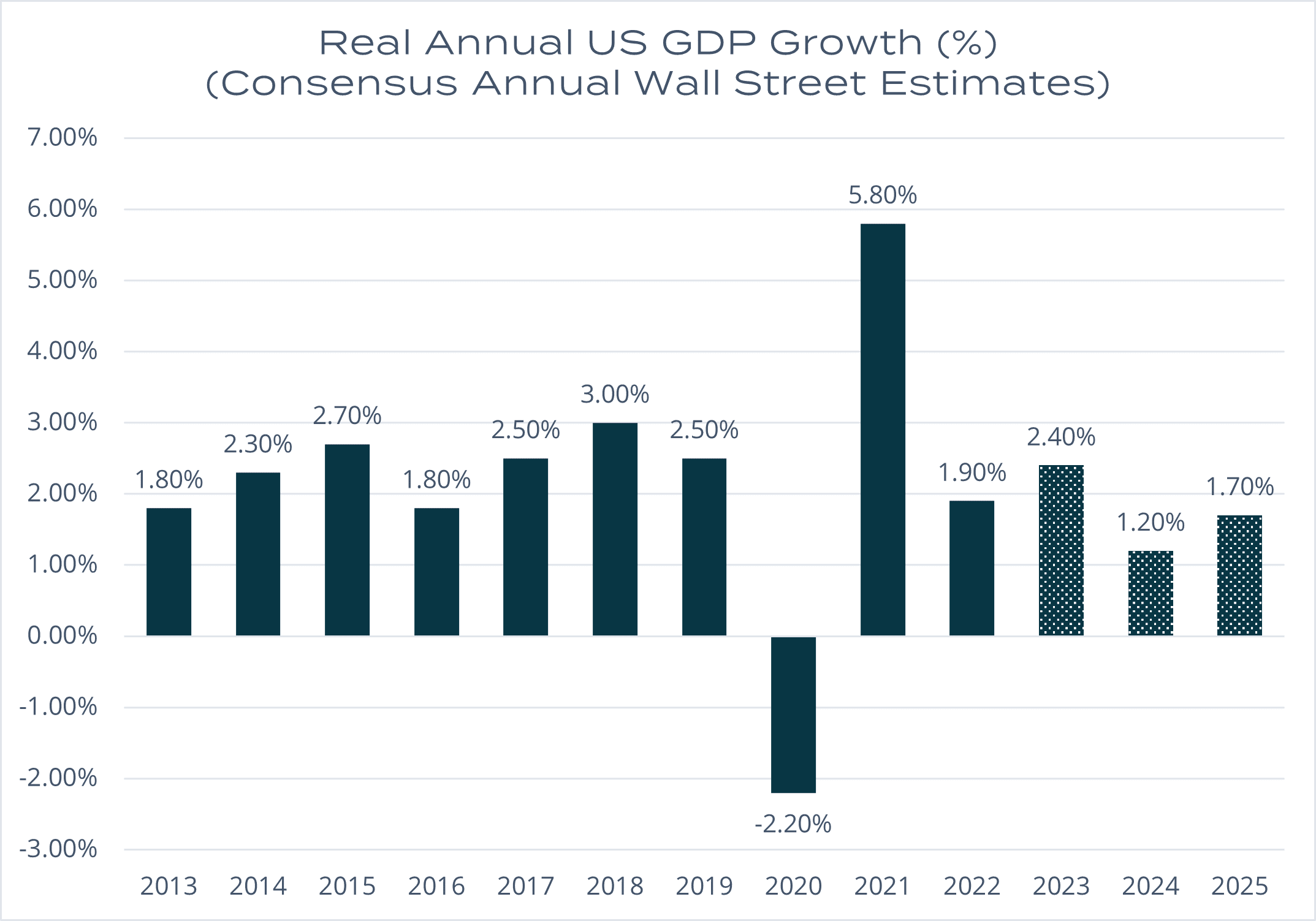

Looking ahead, it’s likely that the lagged impact of the Fed’s restrictive monetary policy could begin to show up in the economic data. For example, U.S. GDP growth is likely to settle below long-term trends and could go negative in the coming quarters.

After outgrowing expectations in 2023, most economists expect 2024 GDP growth to come in at 1.20%, versus the 50-year average growth rate of 2.75%, which would reflect a “soft landing” for the U.S. economy.

However, the longer interest rates stay elevated, the more potential damage they can do to growth expectations. For example, the longer rates stay higher the greater the risk that companies will need to refinance their debt at materially higher interest rates, which could hurt their bottom lines. In addition, higher rates would negatively impact consumers’ purchasing power.

Disinflation & Margin Pressure Put Current Projections at Risk

Corporate margins also may come under pressure in 2024, as disinflationary trends impede pricing power, causing the consumer to become more discerning and putting current earnings growth expectations at risk. Ultimately, equity market prices typically follow the path of corporate earnings.

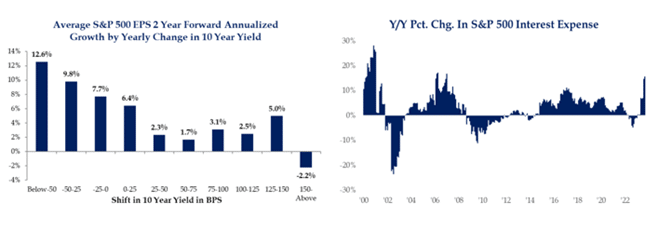

The market currently expects earnings to grow by 12% per year for the next two years. The market may react negatively if earnings don’t meet those expectations.

Revenue growth is (for the market as a whole) heavily influenced by the backdrop of economic activity (or GDP growth expectations). As mentioned, most analysts feel that the economy will slow in 2024, making revenue growth more difficult. In addition, disinflationary trends may make it more difficult for companies to grow revenue. A substantial portion of their growth amid the inflationary environment of the last few years was merely passing through higher prices to consumers. That gets more difficult when inflation slows and the consumer becomes more discerning.

However, because the market predicts earnings will grow double digits next year, despite falling revenue growth, that puts a lot of pressure on margin expansion and the likelihood of achieving double-digit earnings growth. However, margins may be under pressure, particularly with most companies dealing with higher interest expense.

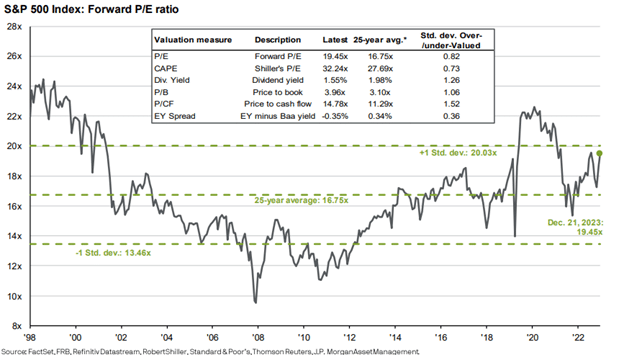

In summary, given that valuations are already above historical averages and interest rates could potentially stay elevated for a while, there is a lot resting on corporate earnings growth to support material market gains over the next year.

Current Market Projection of Fed Funds Sits Well Below Fed Guidance

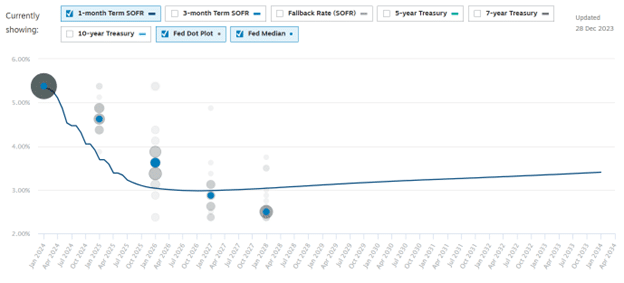

The market is calling for the Fed to begin cutting rates in the first half of 2024, which has been the key driver of the recent rally in the markets. Specifically, 125 basis points (or 1.25%) of interest rate cuts are currently priced into the futures curve for 2024.

The Fed updated its summary of economic projections in December and is now suggesting it will cut rates three times in 2024. That said, the gap between the Fed and the market is just as wide as it was prior to the updated guidance. After hearing the “dovish” rhetoric from the Fed during the December meeting, the market adjusted its expectations and is now calling for more than six cuts in 2024.

Bottom line, the Fed is calling for a 2024 year-end Fed funds rate of 4.625%, versus the market’s projection of 3.75%, a very wide gap. Below is a helpful graphic that lines up market expectations versus Fed guidance.

The gap in expectations creates risk for the market and increases the likelihood of volatility. Among the potential drivers of financial market returns in 2024, none is likely to have a greater influence than the path of Fed policy decisions. We will of course be watching this very closely.

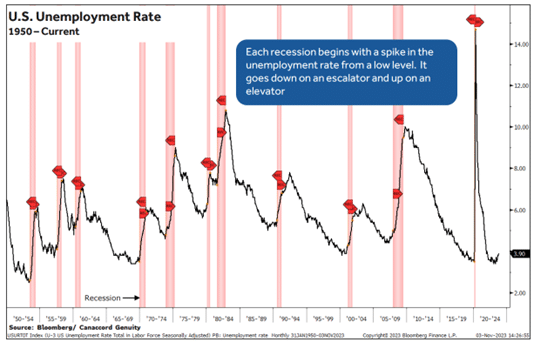

The U.S. Unemployment Rate Rarely Moves Sideways for Long

Thus far, Fed policy has worked to lower inflation without negatively impacting the labor market. That will be tested in 2024 and is perhaps the central issue related to U.S. economic growth expectations in 2024. If the labor market stays tight, we are likely to experience a “soft landing” in the economy. Afterall, jobs are the lifeblood of consumer income and consumer spending makes up more than 2/3 of economic activity.

In normal cycles, restrictive policy puts pressure on growth and corporate profits, incentivizing employers to reduce their labor force (a big expense line item). We have not seen this play out yet, but if it does (which historically it has), it’s likely to happen hard and fast.

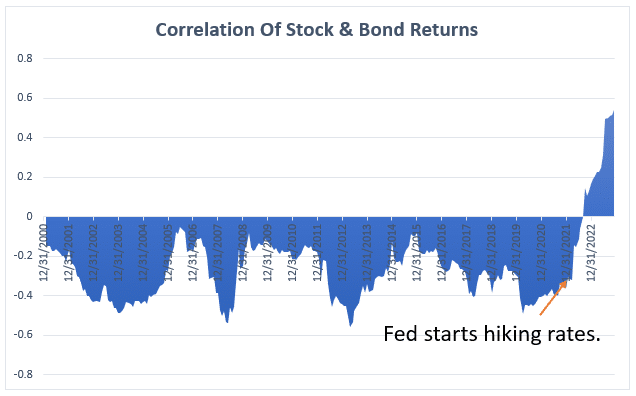

The Correlation of Stock and Bond Returns are Set to Normalize In 2024

Since the beginning of the current Fed interest rate-hiking cycle, fixed income duration has not helped to diversify equity risk. Historically, correlations between stocks and bonds have been negative, meaning that when one went up the other went down. However, in the last couple of years, because of the Fed tightening, the relationship between stock and bond prices turned positive. In other words, owning bonds usually mitigates the risk of owning stocks. However, in the most recent environment, higher interest rates hurt both stock and bond returns.

With the interest rate-hiking cycle potentially ending, fixed income duration is likely to once again diversify equity risk. We expect correlations to begin normalizing back into negative territory, which is an important consideration for portfolio construction.

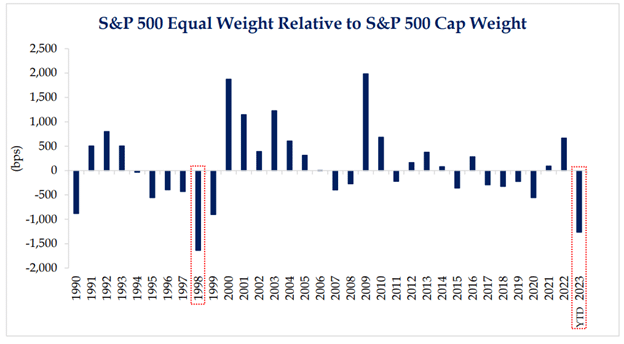

Equity Market Dispersion Has Been Very Wide

In retrospect, 2023 shaped up to be the worst relative year for the average stock since 1998/1999 (pre-tech bubble), outside of the Magnificent 7 referenced earlier. However, it’s worth noting that the average stock at that time went on to outperform for nearly the entirety of the next decade. Market performance has tended to broaden out following periods of heavy performance concentration.

The takeaway here is where you invest within the equity market matters. The variance of returns between style, size, and region has been very wide in recent years and may continue. It’s difficult to get this right with any level of persistency, and you can be overly punished by leaning too far the wrong way. Therefore, our approach is to maintain a balanced exposure across performance factors (style, size and region).

When just a handful of stocks (again, the Magnificent 7) are responsible for most of the equity market’s gains, that market becomes more vulnerable to a downturn if a few of the “heavyweights” fall. Thankfully, we believe that growth opportunities in the global equity market are likely to broaden in the year to come, lessening the dependence of market performance on a few outliers.

We foresee that several major growth themes (e.g. artificial intelligence, cryptocurrencies and weight-loss drugs to name a few) will be tested in 2024, with expectations already very high. Roughly 80% of recent S&P returns are attributable to just 10 companies. While those stratospheric valuations reflect a good deal of optimism, they also can’t afford to disappoint. As stated above, we believe the concentration of stock performance will become more widespread in the next year.

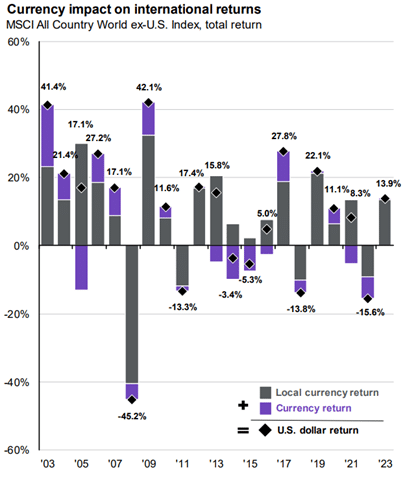

A Weaker Dollar Is Favorable for International Equities

Fluctuations in the value of the dollar versus other currencies can have meaningful implications for international equity performance. Looking ahead, the dollar may come under pressure as interest rates decline and growth slows relative to non-U.S. economies.

The main takeaway is that the potential decline in the dollar gives us more confidence in our exposure to non-US equities.

Further, there are other fundamental factors that are favorable for non-U.S. stocks, such as cheaper valuations, lower growth expectations, and reversion to the mean regarding relative performance versus U.S. stocks.

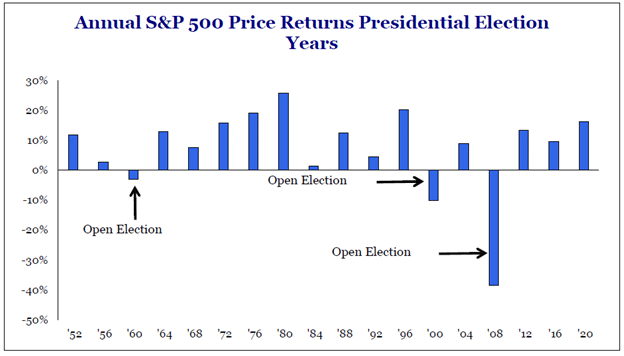

The Presidential Election Will Likely Breed Volatility

The upcoming presidential election is shaping up to be like none other in our lifetimes. While there are a tremendous number of unknowns, we can take solace in knowing that the S&P 500 has not declined in a presidential re-election year since the 1950s. Furthermore, stocks tend to perform better in presidential re-election years than open elections. However, while the 2024 presidential election may not ultimately impact market returns, it is likely to breed volatility as we move closer to election day.

Conclusion

It’s been a long and hard fight, but the rate of inflation appears to be declining to a point at which the Fed will feel comfortable cutting interest rates in 2024. Thus far, policymakers have managed to quell inflation without any meaningful impact on employment. It’s worth pointing out, however, that the job is not done yet, and it is no easy feat given there are so few examples of sticking a “soft landing” following monetary tightening of this magnitude.

While the consumer proved to be remarkably resilient in 2023, we question the sustainability of demand and remain concerned that unemployment trends may weaken, causing a more material economic contraction than what’s priced into the markets. With this in mind, all eyes are on the health of the labor market in 2024.

With respect to the markets, major growth themes will likely be tested in 2024, as will the companies that dominate them. The ability of these “big growers” to meet expectations will ultimately dictate whether earnings projections for the market are too high. It’s worth remembering that concentrated markets can be fragile markets. With that understanding, earnings growth expectations remain elevated as we head into 2024 and may prove to be too optimistic given the lagged (dampening) effects of policy tightening. Thankfully, we believe that growth opportunities in the equity market are likely to broaden out in the years to come, and in light of that expectation, we plan to keep our equity exposure balanced among style, size and regional exposures.

Finally, the 2024 presidential election may not ultimately impact market returns, but it is likely to present an additional source of market volatility as we move though the year.

Disclosures

Investment advisory services offered by Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

Colossal IT Outage Makes a Bad Week Worse for Big Tech