Market Commentary

Broader Market Held Firm Despite a Crack in the AI Trade

by Sequoia Financial Group

by Sequoia Financial Group

All major U.S. stock indices fell last week, ending a remarkable run of nine straight weekly gains for the S&P 500. But the headline numbers hide an unusually lopsided story. The Dow Jones Industrial Average slipped just 0.3 percent, while the technology-heavy NASDAQ Composite tumbled 4.7 percent and the broad S&P 500 fell 2.6 percent. The performance gap comes down to what each index owns: the NASDAQ and S&P are dominated by a handful of giant technology companies – the so-called “Magnificent Seven,” names like Nvidia (ticker: NVDA), Apple (AAPL), and Microsoft (MSFT) – whereas the Dow holds fewer of them. In fact, the “equal-weight” S&P 500, which treats every company the same, fell only about 0.5 percent. In plain terms, the average stock held up fine; the damage was concentrated in the market’s largest, most AI-focused names.

The spark was chipmaker Broadcom (ticker: AVGO), whose products help power AI computing. Its earnings were solid, but its forecast fell short of investors’ lofty expectations, and the disappointment rippled across the semiconductor group – the index of chip stocks suffered its worst single day since the early-pandemic crash of March 2020. Having climbed so far, so fast – technology recently traded near its most expensive level in a decade – AI stocks needed only a small letdown to trigger profit-taking.

Concerns about supply added to the unease. Meta Platforms (ticker: META), the parent of Facebook and Instagram, signaled it might raise tens of billions of dollars in new stock to fund its AI ambitions. A wave of large new stock offerings is also coming to market, including the eagerly awaited initial public offering (IPO) of Elon Musk’s SpaceX next week. Because more shares for sale can weigh on prices, investors are left to wonder whether the market can absorb so much at once.

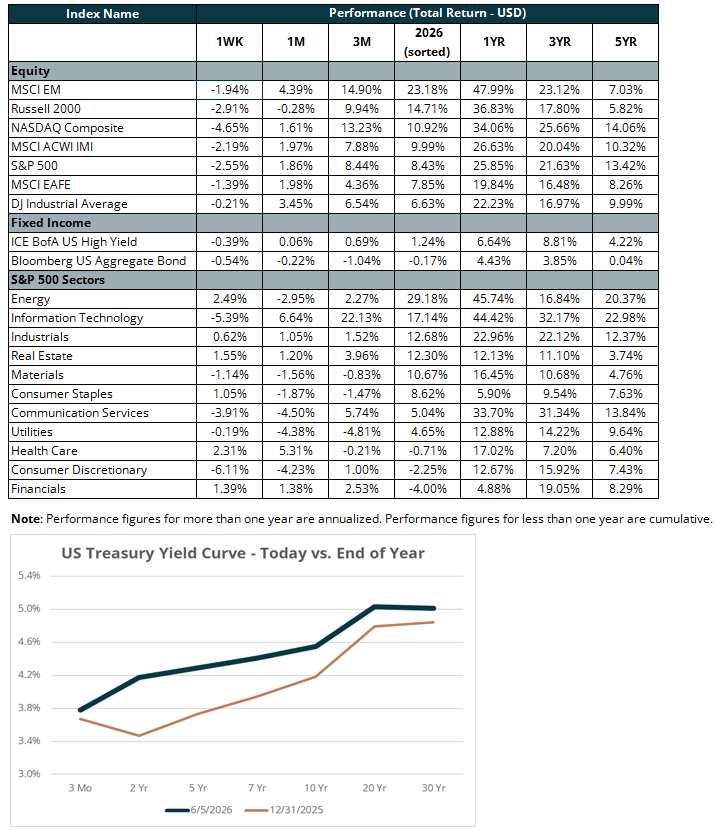

Bonds and gold offered little shelter. On Friday, the government reported that employers added 172,000 jobs in May, roughly double what economists expected. A strong labor market is good news for the economy, but it lowers the odds that the Federal Reserve will cut interest rates soon. That pushed the yield on the 10-year U.S. Treasury note up to 4.54 percent; because bond prices fall when yields rise, bonds declined as well. Gold, which often rises when stocks fall, instead dropped about five percent for the week, as higher interest rates and a stronger U.S. dollar made the metal – which pays no interest – less appealing to hold.

The coming week will test whether this was a healthy pause or something deeper. Investors will watch two key inflation reports – the Consumer Price Index (CPI) on Wednesday and the Producer Price Index (PPI) on Thursday – for clues about the Fed’s next move ahead of its June 17–18 policy meeting. Apple hosts its annual Worldwide Developers Conference on Monday, and software giants Oracle (ticker: ORCL) and Adobe (ADBE) report earnings, giving the AI trade a fresh chance to prove its skeptics wrong.

The views expressed represent the opinion of Sequoia Financial Group. The views are subject to change and are not intended as a forecast or guarantee of future results. This material is for informational purposes only. It does not constitute investment advice and is not intended as an endorsement of any specific investment. Stated information is derived from proprietary and nonproprietary sources that have not been independently verified for accuracy or completeness. While Sequoia believes the information to be accurate and reliable, we do not claim or have responsibility for its completeness, accuracy, or reliability. Statements of future expectations, estimates, projections, and other forward-looking statements are based on available information and Sequoia’s view as of the time of these statements. Accordingly, such statements are inherently speculative as they are based on assumptions that may involve known and unknown risks and uncertainties. Actual results, performance or events may differ materially from those expressed or implied in such statements. Investing in equity securities involves risks, including the potential loss of principal. While equities may offer the potential for greater long-term growth than most debt securities, they generally have higher volatility. Past performance is not an indication of future results. Investment advisory services offered through Sequoia Financial Advisors, LLC, an SEC Registered Investment Advisor. Registration as an investment advisor does not imply a certain level of skill or training.

(1)")

")

")

")

Momentum Trade Moves into Bear Market Territory